Top PDF PRICING and STATIC REPLICATION of FX QUANTO OPTIONS

I s an old exam quesion. Acuarial J. Pricing dynamic. Opions and Volailiy Peer A. Abken and Saika Nandi Abken and Nandi are senior economiss in he financial secion of he Alana Fed s research deparmen. V olailiy is a measure of he dispersion of an asse price. E-mail: sven. Insiue of acuarial sciences. In a ypical paricipaing life insurance conrac, he insurance company is eniled o a. Random Walk in -D Random walks appear in many cones: diffusion is a random walk process undersanding buffering, waiing imes, queuing more generally he heory of sochasic processes gambling choosing he bes.

Muliple-choice quesions may coninue on he ne column or page find all choices before making your selecion. Log in Registration. Search for. Size: px. Start display at page:. Sylvia Houston 5 years ago Views:. Similar documents. The fuure opions include hose paying More information.

Credit Index Options: the no-armageddon pricing measure and the role of correlation after the subprime crisis Second Conference on The Mahemaics of Credi Risk, Princeon May , Credi Index Opions: he no-armageddon pricing measure and he role of correlaion afer he subprime crisis Damiano Brigo - Join work More information. The option pricing framework Chaper 2 The opion pricing framework The opion markes based on swap raes or he LIBOR have become he larges fixed income markes, and caps floors and swapions are he mos imporan derivaives wihin hese markes.

More information. We coninue working wihin he Black and Scholes model inroduced in More information. An accurate analytical approximation for the price of a European-style arithmetic Asian option An accurae analyical approximaion for he price of a European-syle arihmeic Asian opion David Vyncke 1, Marc Goovaers 2, Jan Dhaene 2 Absrac For discree arihmeic Asian opions he payoff depends on he price More information.

Modulated Environment. New Pricing Framework: Options and Bonds arxiv Also, More information. Conceptually calculating what a OTM call option should be worth if the present price of the stock is Pricing exotic options. Suppose he fluid conains a conaminan whose concenraion a posiion a ime will be More information. Exotic electricity options and the valuation of electricity generation and transmission assets Decision Suppor Sysems 30 wwwelseviercomrlocaerdsw Exoic elecriciy opions and he valuaion of elecriciy generaion and ransmission asses Shi-Jie Deng a, , Blake Johnson b, Aram Sogomonian c More information.

- le basi del forex trading pdf.

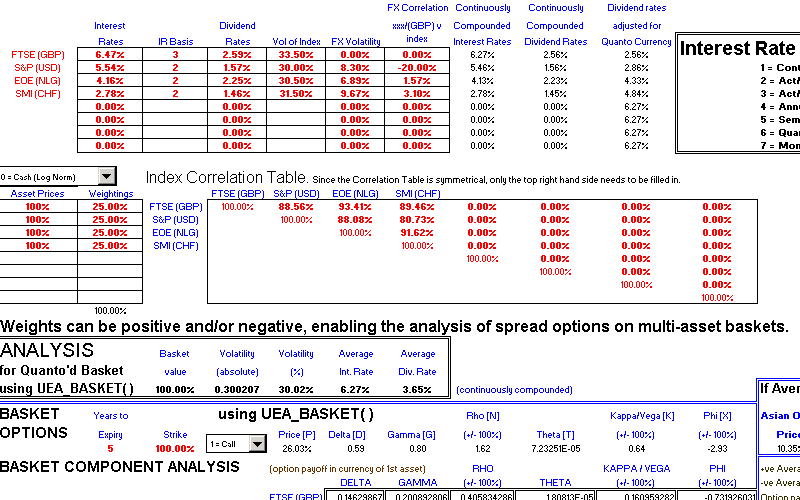

- PRICING and STATIC REPLICATION of FX QUANTO OPTIONS.

- fnb forex buying rate;

- Quanto Basket Option.

Arbitrage-free pricing of Credit Index Options. The no-armageddon pricing measure and the role of correlation after the subprime crisis Arbirage-free pricing of Credi Index Opions. Mehods, Bocconi More information. Sock Transacions Involving Credi More information. Chapter 7.

Andreas Bang Nielsen - Research

A General oluion for ep and Naural More information. Mathematics in Pharmacokinetics What and Why A second attempt to make it clearer Mahemaics in Pharmacokineics Wha and Why A second aemp o make i clearer We have used equaions for concenraion as a funcion of ime. We will coninue o use hese equaions since he plasma concenraions More information. Reproducion or ranscripion More information. An invesor More information.

Nikkei sars calculaing and More information. ARCH Noviyanti a, M. Individual Health Insurance April 30, Pages Individual Healh Insurance April 30, Pages We have received feedback ha his secion of he e is confusing because some of he defined noaion is inconsisen wih comparable life insurance reserve More information.

Description

Credit risk. Lecture of M. SHB Gas Oil. Index Rules v1. Index Descripions The SHB Gasoil index he Index measures he reurn from changes in he price of fuures conracs, which are rolled on a regular More information. Keeping track of time. The model s elements Inroducion Chaper Dynamic D-S dynamic model of aggregae and aggregae supply gives us more insigh ino how he economy works in he shor run. Carbon Trading.

Diederik Dian Schalk Nel. Capacitors and inductors Capaciors and inducors We coninue wih our analysis of linear circuis by inroducing wo new passive and linear elemens: he capacior and he inducor. All he mehods developed so far for he analysis of linear More information. Working Paper On the timing option in a futures contract.

The approach draws on he faciliies More information. European option prices are a good sanity check when analysing bonds with exotic embedded options. Pricing dynamic More information. V olailiy is a measure of he dispersion of an asse price More information. In a ypical paricipaing life insurance conrac, he insurance company is eniled o a More information. Random Walk in 1-D.

The More information. Option Valuation. To make this website work, we log user data and share it with processors. To use this website, you must agree to our Privacy Policy , including cookie policy. I agree. For a better experience, please enable JavaScript in your browser before proceeding. You are using an out of date browser. It may not display this or other websites correctly. You should upgrade or use an alternative browser. Quanto options.. I am trying to understand the intuition behind how quants are hedged.. So the trader is short gamma and will make losses on his delta hedge..

Alright so in this example an American investor wants to own an Australian equity and get paid the return that equity experiences in the local market, but in USD. If it's zero, he won't deal any FX option and just hedge out the FX exposure with forwards as it develops. Once he marks his correlation at what he think it will actually realize until maturity of the quant0 and then hedges his FX option exposure according to that correlation, his unhedged risk becomes purely being wrong about his correlation assumption as that will have him mis-hedged on his gamma. There's not really a way to hedge this exposure, so traders will price the quanto option using a conservative assumption for what the correlation could be, and then risk manage according to fair value, hoping to earn the difference in price between where they bid or offered the correlation and where they actually believe it will realize.

Post reply. Similar threads W. Partial Derivatives of Index Straddle w. Index Constituents.