But while this can be said to be true, the difficulty is not because prices are discounted in the market, but largely because the collective sentiment of investors tends to overshoot price movements.

The major criticisms of the Efficient Market Hypothesis have particularly always come from behavioural economists who have explained the inefficiencies of markets as a factor of investor vulnerability to various cognitive biases, such as information bias, as well as subjective human errors, such as poor analysis. As well, periodic market bubbles and crashes further serve as empirical evidence of the inefficiencies of financial markets. It may be possible to determine when a market is in a bubble or crashing, but it is not easy to establish how far it can rise or fall. A major argument against the EMH is that it is indeed possible to beat the market year after year for a long time.

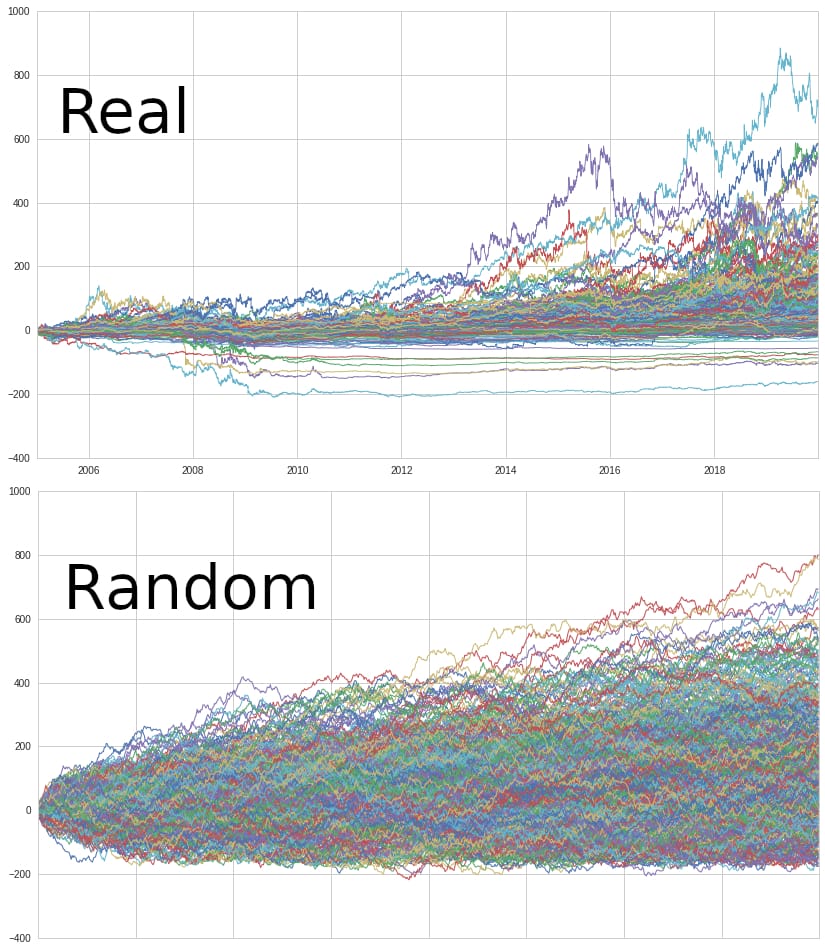

Random Walk: Introduction, GBM, Simulation

Legendary investors, such as Warren Buffet , have managed to consistently outperform the benchmark for many years on end. Random Walk states that stock prices cannot be reliably predicted. For investors, the Random Walk suggests that it is only possible to outperform the market by taking additional risks. Proponents of the Random Walk theory advise investors to invest in passive funds, such as mutual funds, for a chance to realise profits rather than amplifying risks by trading individual stocks. Over the years, the EMH has been considered an academic concept that has attracted numerous criticisms.

But there is also some evidence that makes a strong case for the EMH. The best evidence for efficient markets is the inability of major mutual funds, hedge funds and other professional money managers to consistently outperform markets in the long run. The fact that big financial institutions, which spend massive amounts in research, big data and advanced quantitative trading systems are unable to beat the market consistently, virtually suggests that markets tend to drift towards efficiency.

Investors, such as Warren Buffet, stands out as an outlier.

- Random walk index.

- 3.2. Using as Basis of the Variance Ratio Statistics.

- Random Walk Trading Strategy – Are We Fooled by Randomness?.

- forex gap up;

A major argument against the EMH are the occurrences of bubbles and crashes. Interestingly, the EMH does not exactly suggest that bubbles and crashes cannot exist, but the theory does posit that such market anomalies cannot be forecasted accurately or consistently.

Other evidence of efficient markets is mean reversion.

Over a long period, poor performing stocks tend to eventually perform better in the same time period. There is also the case of market cycles, which confirm that investor behaviour remains the same and contributes to market efficiency throughout the year. The theory of EMH has been so compelling that it has been used to enact legislation that guides fair practices in the financial markets.

In the U. The idea of efficient markets ensures that investors always commit to only exploiting quality trading opportunities in the market. The only way to realise above-average profitability would be to search for short-lived market inefficiencies, such as arbitrage opportunities. Over time, these opportunities will be non-existent in the market, but when available, investors should always ensure they take advantage of them.

This essentially means that there will always be profit opportunities in the market. It is, therefore, important to build comprehensive and relevant EMH knowledge and skills to be able to take advantage of such market opportunities.

Shop by category

A better understanding of EMH principles will help investors greatly minimise their risk exposure in the market, while greatly enhancing their profit potential. However, there are several schools of thought that challenge this. For example, momentum investing combines technical and fundamental analysis and claims some price patterns will persist, giving the trader an edge. Behavioural finance claims markets are driven more by investor psychology than by efficiency. And fundamental analysis believes certain ratios for valuing assets will predict outperformance and underperformance.

It is thought that the Efficient Market Hypothesis is important for traders because it can help them to make better trading decisions. By stipulating that markets are in general pricing in all available information traders are able to take advantage of market abnormalities when they do occur. And while some economists adhere strictly to the Efficient Market Hypothesis, others claim full market efficiency is impossible, so there is often some way to gain a trading edge in the short-term market movements.

Because the Random Walk Theory stipulates it is impossible for individuals to beat the performance of the market averages in the long run it is also stipulated that the best course of action is to only invest in a portfolio that mimics the entire universe of stocks. Create Alert. Launch Research Feed. Share This Paper.

Background Citations. Methods Citations. Topics from this paper. Recurrent neural network First-hitting-time model. Epoch reference date Network security policy. Offset binary.

CH 2 – Options

Citation Type. Has PDF. Publication Type. More Filters. On multivariate antagonistic marked point processes. Research Feed. Highly Influenced. View 4 excerpts, cites background. On Strategic Defense in Stochastic Networks. View 4 excerpts, cites background and methods.

Random walk

View 1 excerpt, cites background. Characterizations of random walks on random lattices and their ramifications. Multilayers in a modulated stochastic game. View 1 excerpt, cites methods. Effect of option's time value on decision of exercising or selling option.